|

The Week Ahead: Highlights

Asia-Pacific Preview

China Economic Data Returns

By Brian Jackson, Econoday Economist

Chinese data will be the highlight of the Asia-Pacific

calendar after the normal holiday-related gap in the release schedule in

February. Trade data for January and February combined will provide an

indication of how activity has been at the start of the year, while inflation

data for February will likely show further subdued price pressures. The annual

session of the National People's Congress, which started last week, will

conclude and endorse the policy stability set out by Premier Li Qiang at the

opening of the session.

Business and consumer confidence data in Australia will

provide an indication of the impact on sentiment of the Reserve Bank of

Australia's decision to increase policy rates last month. South Korean GDP,

Indian inflation, and Taiwanese trade data are also scheduled for

release.

Europe Preview

Iran War Dominates Attention

By Marco Babic, Econoday Economist

While the week ahead is quiet in terms of data releases for

Europe, there is no getting around the upheaval caused by last week's attacks

on Iran by the US and Israel. Final CPI data for February are coming from

Germany, France, and the Netherlands, where preliminary results showed still

subdued inflation for Germany and the Netherlands. In France, however,

month-on-month inflation flipped dramatically from a 0.3 percent decline in

January to a 0.7 percent gain in February.

With the usual caveat of one month does not a trend make, the results for

France could be a harbinger of higher prices to come. Already industries are

reporting higher input costs which they are starting to pass downstream. With

the conflict in the Middle East now spreading, oil prices are moving higher which

will already likely manifest itself in the March data.

To make matters worse, there were some indications that reluctant European

consumers were starting to loosen their purse strings. They were able to do

this precisely because energy prices had been subdued. This is no longer likely

to be the case, and the higher costs will eat into discretionary purchasing

power and have a negative impact on GDP should there be no swift resolution to

the flighting.

Among other major indicators, Germany reports industrial

production for January, with Italy and the Eurozone releasing their production

statistics on Friday. In December, production ended the year on a negative

note, and there are no concrete signs emerging from other reports to suggest

there will be any significant recovery in January. While in some countries,

businesses have become more optimistic, the lack of new orders continues to be

of concern.

Friday's US employment report which showed the economy shedding 92,000 jobs

with the unemployment rate rising to 4.4 percent will further add to worries

about the underpinnings of the global economy

US Preview

Inflation Reports in Focus in Runup to FOMC Meeting

By Theresa Sheehan, Econoday Economist

The March 9 week is in the lead up to the March 17-18 FOMC

meeting. The communications blackout period around the meeting begins at

midnight on Saturday, March 8 and runs through midnight on Thursday, March 19. Fed policymakers will not be providing comment regarding the outlook for

monetary policy during that time. Fed Chair Jerome Powell's semiannual monetary

policy testimony is late and has yet to be scheduled. It is highly unlikely to

take place in the March 9 week and as such now won't be until after the FOMC

meeting.

The economic data release schedule has a number of reports

pertinent to the upcoming FOMC deliberations. However, at least some of the

data is already out of date after the US initialed its war on Iran on February

28. Oil prices are already rising sharply and not done. The effect on inflation

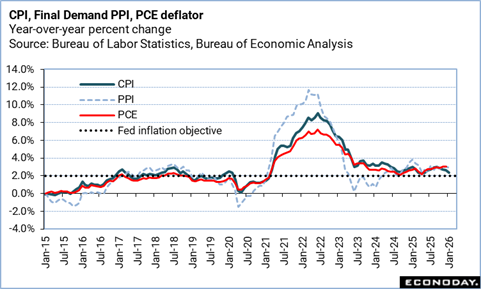

in the US is not yet realized. The release of the February CPI report at 8:30

ET on Wednesday and Final Demand PPI at 8:30 ET on Thursday will not reflect

the movement in the first days of March. The PCE deflator for January is at

8:30 ET on Friday and is too old to provide clarity for the current situation.

Fed policymakers will once again have to wait and see where the data takes us

before the April 28-29 FOMC meeting.

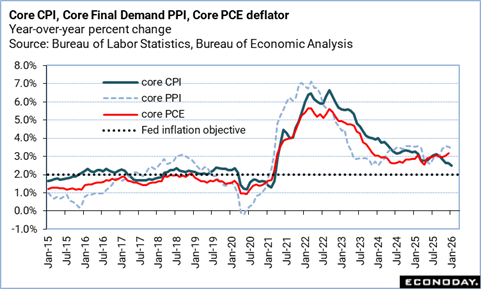

The impacts from higher tariffs imposed early in 2025 were

fading but now the inflation reports face a new challenge. Moreover, the

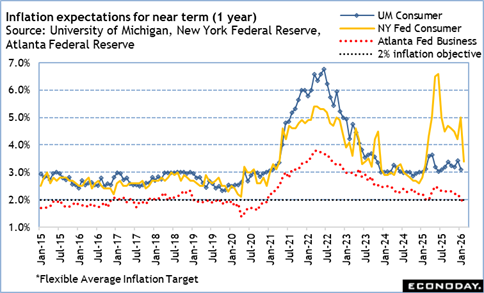

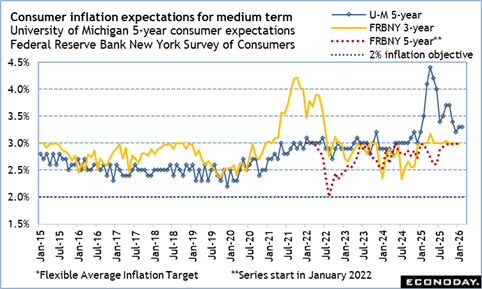

stability of inflation expectations will be rattled - especially in the short

term - by the higher oil prices. While 1-year inflation expectations in March

will certainly take a jump, the question is if successive blows to getting

inflation back to the Fed's 2 percent objective will finally unanchor

expectations for the longer term. The University of Michigan's Survey of Consumers

read on inflation expectations for early March will be one of the first clues.

The Week Ahead: Econoday Consensus Forecasts

Monday

China CPI for February (Mon 0930 CST; Mon 0130 GMT;

Sun 2030 EDT)

Consensus Forecast, Y/Y: 0.7%

Consensus Range, Y/Y: 0.5% to 0.9%

CPI expected to pick up to 0.7 percent on year in the

February report after a marginal 0.2 percent uptick in January.

China PPI for February (Mon 0930 CST; Mon 0130 GMT;

Sun 2030 EDT)

Consensus Forecast, Y/Y: -1.1%

Consensus Range, Y/Y: -1.2% to -1.0%

Deflation to slow to minus 1.1 percent in February from

minus 1.4 percent in January.

Germany Industrial Production for January (Mon 0800

CET; Mon 0700 GMT; Mon 0300 EDT)

Consensus Forecast, M/M: 1.1%

Consensus Range, M/M: 0.9% to 1.5%

Consensus Forecast, Y/Y: -0.7%

Consensus Range, Y/Y: -0.8% to -0.2%

Output expected to rebound by 1.1 percent on the month in

January after a 1.9 percent drop in December. On year, the consensus sees a

decline of 0.7 percent after the 0.5 percent decrease in December.

Tuesday

South Korea GDP for Fourth Quarter (Tue 0800 KST; Mon

2300 GMT; Mon 1900 EDT)

Consensus Forecast, Y/Y: 1.5%

Consensus Range, Y/Y: 1.5% to 1.7%

Growth rate seen flat at 1.5 percent on year in Q4.

Japan Household Spending for January (Tue 0830 JST; Mon

2330 GMT; Mon 1930 EDT)

Consensus Forecast, M/M: 0.6%

Consensus Range, M/M: -0.4% to 2.9%

Consensus Forecast, Y/Y: 1.8%

Consensus Range, Y/Y: 0.6% to 5.2%

Household spending is expected to rise 1.8 percent on the

year in January after declining 2.6 percent a month earlier. December's fall

was partly a reaction to the previous month's jump in automobile purchases. In

addition, there was a drop in another volatile item, home maintenance and

repairs. Even the core measure of expenditures (excluding housing, motor

vehicles and remittances) fell 1.5%, indicating that consumers remain frugal.

On a month-on-month basis, household spending is expected to

rise 0.6 percent in January, rebounding from a 2.9 percent fall a month

earlier.

Japan GDP for Fourth Quarter (Tue 0850 JST; Mon 2350

GMT; Mon 1850 EDT)

Consensus Forecast, Q/Q: 0.3%

Consensus Range, Q/Q: 0.2% to 0.4%

Consensus Forecast, Y/Y: 0.3%

Consensus Range, Y/Y: 0.2% to 0.4%

The country's revised Q4 GDP is expected to rise for the

first time in two quarters, increasing 0.3 percent on the quarter compared with

the preliminary reading of 0.1 percent that was released on February 16. On an

annualized basis, the revised GDP is expected to grow 1.3 percent, up from the

preliminary estimate of 0.2 percent.

Germany Merchandise Trade for January (Tue 0800 CET; Tue

0700 GMT; Tue 0300 EDT)

Consensus Forecast, Balance: E15.4 B

Consensus Range, Balance: E15.4 B to E 15.7 B

The surplus is expected to narrow to E15.4 billion in

January from E17.1 billion in December.

US NFIB Small Business Optimism Index for February (Tue

0600 EDT; Tue 1000 GMT)

Consensus Forecast, Index: 99.7

Consensus Range, Index: 99.1 to 100.0

Business sentiment expected edge up marginally to 99.7 from

99.3 in the previous month.

US Existing Home Sales for February (Tue 1000 EDT; Tue

1400 GMT)

Consensus Forecast, Annual Rate: 3.88 M

Consensus Range, Annual Rate: 3.81 M to 3.98 M

Sales remain in doldrums, expected at 3.88 million unit rate

versus 3.91 million a month earlier.

Wednesday

Japan PPI for February (Wed 0850 JST; Tue 2350 GMT; Tue

1950 EDT)

Consensus Forecast, M/M: 0.1%

Consensus Range, M/M: -0.1% to 0.2%

Consensus Forecast, Y/Y: 2.1%

Consensus Range, Y/Y: 2.0% to 2.3%

Japan's producer inflation is expected to rise on the year

for a 60th consecutive month, or five years, in February amid gains in

industrial metals prices and an uptrend in crude oil prices as geopolitical

tensions grow in the Middle East, but the pace of growth is expected to be the

slowest in nearly two years.

Producer inflation, measured by the corporate goods price

index (CGPI), is seen rising 2.1 percent on the year in February, slowing from

a 2.3 percent increase in the previous month, when the pace of growth eased to

the weakest since April 2024.

On a month-on-month basis, the CGPI is seen rising a slim

0.1 percent, marking a sixth straight monthly increase after a 0.2 percent gain

in January.

Germany CPI for February (Wed 0800 CET; Wed 0700 GMT;

Wed 0300 EDT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: 0.2% to 0.2%

Consensus Forecast, Y/Y: 1.9%

Consensus Range, Y/Y: 1.9% to 1.9%

Consensus Forecast, HICP - M/M: 0.4%

Consensus Range, HICP - M/M: 0.4% to 0.4%

Consensus Forecast, HICP - Y/Y: 2.0%

Consensus Range, HICP - Y/Y: 2.0% to 2.0%

No revision expected from the flash with CPI up 0.2 percent

on month and 2.0 percent on year.

US CPI for February (Wed 0830 EDT; Wed 1230 GMT)

Consensus Forecast, CPI - M/M: 0.3%

Consensus Range, CPI - M/M: 0.2% to 0.3%

Consensus Forecast, CPI - Y/Y: 2.4%

Consensus Range, CPI - Y/Y: 2.4% to 2.6%

Consensus Forecast, Ex-Food & Energy - M/M: 0.2%

Consensus Range, Ex-Food & Energy - M/M: 0.2% to 0.3%

Consensus Forecast, Ex-Food & Energy - Y/Y: 2.5%

Consensus Range, Ex-Food & Energy - Y/Y: 2.4% to 2.5%

Inflation chugs along about the same as usual with CPI up

0.3 percent on the month and 2.4 percent on year versus 0.2 percent and 2.4

percent a month earlier.

Thursday

Canada Merchandise Trade for January (Thu 0830 EDT;

Thu 1230 GMT)

Consensus Forecast, Balance: -C$0.9 B

Consensus Range, Balance: -C$1.0 B to -C$0.8 B

The trade balance is seen barely in deficit at C$0.9 billion

in January versus C$1.308 billion in December.

US Housing Starts and Permits for January (Thu 0830 EDT;

Thu 1230 GMT)

Consensus Forecast, Starts - Annual Rate: 1.340 M

Consensus Range, Starts - Annual Rate: 1.309 M to

1.370

Consensus Forecast, Permits - Annual Rate: 1.410 M

Consensus Range, Permits - Annual Rate: 1.347 M to

1.433 M

Starts expected to sag to 1.340 million in January from

1.404 million I December and permits seen at 1.410 million versus 1.448

million.

US International Trade in Goods and Services for January (Thu

0830 EDT; Thu 1230 GMT)

Consensus Forecast, Balance: - $67.9 B

Consensus Range, Balance: -$80.0 B to -$65.0 B

The deficit expected narrower at $67.9 billion from $70.3

billion in December.

US Jobless Claims for Week 03/07 (Thu 0830 EDT; Thu 1230

GMT)

Consensus Forecast, Initial Claims - Level: 217K

Consensus Range, Initial Claims - Level: 208K to 220K

Claims seen rising to 217K after holding at 213K in the

previous week.

Friday

France CPI for February (Fri 0745 CET; Fri 0645 GMT;

Fri 0245 EDT)

Consensus Forecast, M/M: 0.7%

Consensus Range, M/M: 0.7% to 0.7%

Consensus Forecast, Y/Y: 1.0%

Consensus Range, Y/Y: 1.0% to 1.0%

The consensus looks for no revision in the final from the

flash with CPI up 0.7 percent on month and 1.0 percent on year.

Eurozone Industrial Production for January (Fri 1100

CET; Fri 1000 GMT; Fri 0600 EDT)

Consensus Forecast, M/M: 0.5%

Consensus Range, M/M: 0.5% to 0.9%

Consensus Forecast, Y/Y: 1.4%

Consensus Range, Y/Y: 1.3% to 1.5%

Output expected up 0.5 percent on month and 1.4 percent on

year in January after falling 1.4 percent on the month and rising 1.2 percent

on year in December.

Canada Labour Force Survey for February (Fri 0830 EDT;

Fri 1230 GMT)

Consensus Forecast, Employment - M/M: 10K

Consensus Range, Employment - M/M: -15K to 50K

Consensus Forecast, Unemployment Rate: 6.6%

Consensus Range, Unemployment Rate: 6.6% to 6.7%

Jobs expected up by 10K after declining 25K a month earlier

as employment reflects a weak, uncertain economy. The jobless rate is expected

up to 6.6 percent from 6.5 percent a month ago.

Canada Manufacturing Sales for January (Fri 0830 EDT;

Fri 1230 GMT)

Consensus Forecast, M/M: -3.3%

Consensus Range, M/M: -3.3% to -3.3%

As usual, forecasters agree with Statistics Canada's

preliminary estimate which calls for a drop of 3.3 percent on the month in

January after rising 0.6 percent in December.

US GDP for Fourth Quarter (Fri 0830 EDT; Fri 1230

GMT)

Consensus Forecast, Quarter over Quarter - Annual Rate:

1.4%

Consensus Range, Quarter over Quarter - Annual Rate: 1.3%

to 1.5%

The consensus sees no revision from a growth rate of 1.4

percent in the previous report.

US Durable Goods Orders for January (Fri 0830 EDT;

Fri 1230 GMT)

Consensus Forecast, Durable Goods Orders - M/M: 0.5%

Consensus Range, Durable Goods Orders - M/M: -2.0% to

1.7%

Orders expected up 0.5 percent after falling 1.4 percent on

weak aircraft orders a month earlier.

US Personal Income and Outlays for January (Fri 0830

EDT; Fri 1230 GMT)

Consensus Forecast, Personal Income - M/M: 0.5%

Consensus Range, Personal Income - M/M: 0.2% to 0.6%

Consensus Forecast, Personal Consumption Expenditures -

M/M: 0.3%

Consensus Range, Personal Consumption Expenditures - M/M:

0.0% to 0.4%

Consensus Forecast, PCE Price Index - M/M: 0.3%

Consensus Range, PCE Price Index - M/M: 0.2% to 0.4%

Consensus Forecast, PCE Price Index - Y/Y: 2.9%

Consensus Range, PCE Price Index - Y/Y: 2.7% to 3.0%

Consensus Forecast, Core PCE Price Index - M/M: 0.4%

Consensus Range, Core PCE Price Index - M/M: 0.3% to

0.4%

Consensus Forecast, Core PCE Price Index - Y/Y: 3.0%

Consensus Range, Core PCE Price Index - Y/Y: 3.0% to

3.1%

Income expected to outpace spending with income up 0.5

percent and spending up 0.3 percent on the month.

US Consumer Sentiment for March (Fri 1000 EDT; Fri 1400

GMT)

Consensus Forecast, Index: 56.2

Consensus Range, Index: 53.0 to 57.5

Forecasters expect sentiment nearly unchanged at a

relatively gloomy 56.2 in the initial March report versus 56.6 in the final for

February.

US JOLTS for January (Fri 1000 EDT; Fri 1400 GMT)

Consensus Forecast, Mlns: 6.750

Consensus Range, Mlns: 6.675 to 6.800

The consensus sees job openings back up at 6.750 million in

the delayed January report after a surprise drop to 6.542 million in December.

|