|

The Week Ahead: Highlights

Asia-Pacific Preview

Markets Eye China Inflation Reports with Mideast War

Lifting Fuel Prices

By Brian Jackson, Econoday Economist

Chinese inflation data will be a key focus in

the week ahead with the Iran conflict likely to have an impact

on price pressures.

March data

showed producer price inflation returning to positive

territory for the first time since 2022, and this will likely be

extended in April by higher fuel prices, with PMI survey data published

earlier in the month showing strong growth in input costs.

CPI inflation moderated in March after volatility in the first

two months of the year associated with the timing of lunar new year

holidays, but it remained well above levels recorded over 2025.

In Australia, the NAB business survey will

be watched for any signs of a stabilisation in sentiment after

it showed a very sharp drop last month. The survey's

business confidence index recorded the second largest fall in

survey history in response to the Iran conflict, though its business

conditions index was relatively steady. Last month's survey

also showed a substantial impact form the Iran conflict on cost

pressures. Quarterly wage data will also be published next

week. At their policy meeting this week, officials at the

Reserve Bank of Australia noted capacity pressures in the economy,

with any pick-up in wage growth likely

to reinforce their concerns about the

inflation outlook.

The Iran conflict will also likely impact

India inflation data out next week. CPI inflation rose to

3.4 percent in March, closer to the mid-point of the Reserve Bank of

India's target range of two percent to six percent. WPI inflation

rose even more sharply to 3.9 percent, a three-year high. At the RBI's most

recent policy meeting, held last month, officials highlighted the uncertainty

associated with the Iran conflict and the potential upside risks to inflation

if fuel prices remain high. Nevertheless, they expressed confidence that

"the fundamentals of the Indian economy are on a stronger footing"

and expect underlying price pressures to remain contained. Indian trade data

will also be published next week.

Hong Kong will publish revised GDP data for the three

months to March. The advance estimate showed year-over-year

growth increasing 5.9 percent, the fastest pace in almost five

years. More time PMI survey data, however, indicated contraction in

Hong Kong's economy in April.

Europe Preview

Eurozone GDP in Focus

By Marco Babic, Econoday Economist

The week ahead has final first quarter GDP on offer

Wednesday, and while normally the final result doesn't stray too far from the

preliminary result, the conflict in the Middle East could be a large factor.

The flash results were for a 0.1 percent quarter-on-quarter

increase and a 0.8 percent increase over the first quarter of last year. One

thing to look for will be the contribution from trade and the comparison

between the value and volume measures, where there could be a scenario of

higher nominal results and lower volumes.

With the Mideast conflict now well into its third month,

there is a real risk for contraction in the second quarter which presents a

real dilemma for the European Central bank as it could be facing scenario of

stagflation from lower growth and higher inflation. It almost feels like we're

back in the early 1970's and the days of the oil embargo.

Final inflation data for April are due from Germany, while

saw its annual inflation rate at 2.9 percent in preliminary estimates, and

France where CPI was a more modest 2.2 percent year-on-year. In Italy, CPI

stood at 2.8 percent year-on-year in April. These are levels which will make

the ECB rather uncomfortable as they are all above the 2.0 percent target that

the central bank considers acceptable.

Some observers will likely point out that core inflation is

more moderate. While that may be true, consumers facing much higher energy

costs will likely put off major purchases in the coming months and cut back on

discretionary spending. Not an idea situation for economic growth.

The other major indicator next week is Germany's ZEW

Investor Sentiment Survey for May, which is one of the most forward-looking

European indicators. In April, the current conditions measure fell to minus

73.7 from minus 62.9, while that for the economic situation deteriorated to

minus 17.2 from minus 0.5. ZEW also publishes a measure for Eurozone sentiment

in the same report which will be worth watching.

Europe is clearly still facing major headwinds from the

Middle East conflict which, even if resolved soon, will have a significant

impact on second quarter economic growth.

US Preview

Inflation in Focus What Else?

By Theresa Sheehan, Econoday Economist

The focus in the May 11 week will be on the inflation

indicators CPI at 8:30 ET on Tuesday, final-demand PPI at 8:30 ET on

Wednesday, and the import and export price indexes at 8:30 ET on Thursday. This

isn't the last set of BLS reports on inflation that the FOMC will have to hand

at the June 16-17 meeting. However, the April numbers will shape expectations

for monetary policy as the war on Iran continues to keep energy prices

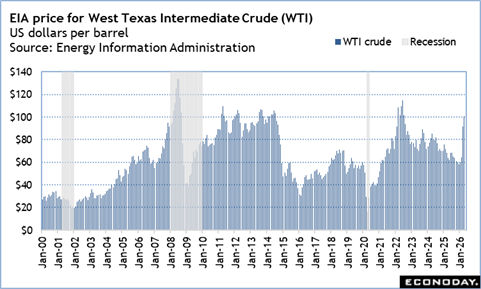

elevated. Oil prices are fluctuating without any sustained downward movement. Even

if the upward movement in prices abates, it will not change in the near term

that households and businesses have fewer dollars to spend on other items. So,

while inflation may level off after the energy-driven inflation in March and

April, spending and investment will still have to deal with the new reality of

higher energy costs.

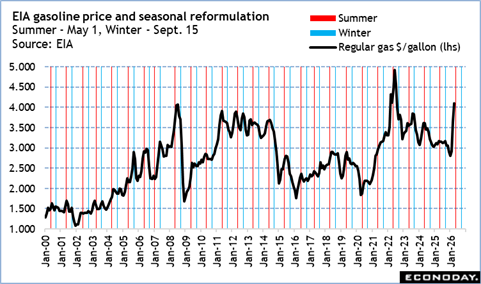

Of particular note for the April CPI numbers is that

gasoline prices have spiked from February. The EIA weekly average for regular

gasoline was $2.924 per gallon in the February 23 week and hit a high of $4.452

per gallon in the May 4 week. There probably won't be a repeat in April of the

month-over-month surge of 21.2 percent in the CPI for gasoline in March, but a

substantial upward move is expected. The seasonal adjustment factors for April

anticipate a rise in gasoline prices associated with the reformulation of

gasoline blends for the summer months which completes by May 1. Still, the

seasonal factors will only partially capture the change in prices at the pump.

The PPI for April should reflect that oil prices were at

their peak during the week that the BLS uses to calculate the energy component.

More importantly, the PPI will provide some clarity about if businesses are

attempting to avoid passing on increased costs to consumers, or if price hikes

are in the works.

The import price index for April will definitely get a boost

from oil prices which are priced in US dollars. There probably won't be a lot

of movement in the non-fuel import price index for goods. What will be more

significant is in the import and export price indexes for air freight and

passenger services. These costs are set to rise due to higher prices for jet

fuels that affect transportation costs.

The Week Ahead: Econoday Consensus Forecasts

Monday

China Merchandise Trade Balance for April (Sunday)

Consensus Forecast, $85.1 Bln

Consensus Range, $82.0 Bln to $86.0 Bln

The surplus is set to rise to $85.1 billion from $55.1 in

March.

China CPI for April (Mon 0930 CST; Mon 0130 GMT; Sun

2130 EDT)

Consensus Forecast, Y/Y: 0.9%

Consensus Range, Y/Y: 0.7% to 1.3%

The consensus looks for CPI up 0.9 percent on year in April

after rising 1.0 percent in March as rising energy prices continue to skew the

numbers higher.

China PPI for April (Mon 0930 CST; Mon 0130 GMT; Sun

2130 EDT)

Consensus Forecast, Y/Y: 1.8%

Consensus Range, Y/Y: 1.5% to 1.9%

The consensus looks for PPI up 1.8 percent on year in April

after rising 0.5 percent in March.

US Existing Home Sales for April (Mon 1000 EDT; Thu 1400

GMT)

Consensus Forecast, Annual Rate: 4.05 M

Consensus Range, Annual Rate: 4.01 M to 4.11 M

Forecasters see sales recovering to an annual 4.05 million

versus a soft 3.98 million in March.

Tuesday

Japan Household Spending for March (Tue 0830 JST; Mon

2330 GMT; Mon 1930 EDT)

Consensus Forecast, M/M: 0.0%

Consensus Range, M/M: -1.4% to 1.5%

Consensus Forecast, Y/Y: -1.7%

Consensus Range, Y/Y: -4.3% to 1.6%

Japan's real household spending is seen falling for a fourth

straight month on the year in March, as higher energy prices and uncertainty

over future supplies amid persistent Middle East tensions weighed on consumer

spending behavior.

Spending by households with two or more persons is forecast

to fall 1.7 percent on the year in March, following a 1.8 percent decline in

February. In February, transportation and communication spending, including

automobile-related expenses, dropped 5.9 percent in real terms, while food

spending, including fish and seafood as well as oils and seasonings, fell 0.5

percent.

Household spending in March is seen dragged down by a

decline in supermarket sales after an increase in February. New passenger car

registrations are also expected to fall, although the pace of decline is likely

to moderate from the previous month.

Spending on both goods and services, based on credit card

usage data, is also seen decreasing in March, although department store sales,

convenience store sales and overall retail sales data showed some improvement.

Reflecting these trends, household spending on a

month-on-month basis is expected to be flat in March after rising 1.5 percent

in February.

Germany CPI for April (Tue 0800 CEST; Tue 0600 GMT; Tue

0200 EDT)

Consensus Forecast, M/M: 0.6%

Consensus Range, M/M: 0.6% to 0.6%

Consensus Forecast, Y/Y: 2.9%

Consensus Range, Y/Y: 2.9% to 2.9%

Consensus Forecast, HICP - M/M: 0.5%

Consensus Range, HICP - M/M: 0.5% to 0.5%

Consensus Forecast, HICP - Y/Y: 2.9%

Consensus Range, HICP - Y/Y: 2.9% to 2.9%

CPI seen up 0.6 percent on month and 2.9 percent on year in

April, unrevised from the flash.

Italy Industrial Production for March (Tue 1000 CEST;

Tue 0800 GMT; Tue 0400 EDT)

Consensus Forecast, M/M: -0.2%

Consensus Range, M/M: -0.4% to 0.0%

Consensus Forecast, Y/Y: 0.3%

Consensus Range, Y/Y: 0.2% to 0.7%

Output expected down 0.2 percent on month and up 0.3 percent

on year in March after rising 0.1 percent on month and 0.5 percent on year in

February.

Germany ZEW Survey for May (Tue 1100 CET; Tue 0900

GMT; Tue 0500 EDT)

Consensus Forecast, Current Conditions: -78.0

Consensus Range, Current Conditions: -78.0 to -76.0

Consensus Forecast, Economic Sentiment: -20.5

Consensus Range, Economic Sentiment: -26.0 to -15.0

With fallout from the Mideast war, sentiment is seen down in

May at minus 78.0 for current conditions and minus 20.5 for economic sentiment

from minus 73.7 and minus 17.2 in April, respectively.

US NFIB Small Business Optimism Index for April (Tue

0600 EDT; Tue 1000 GMT)

Consensus Forecast, Index: 96.1

Consensus Range, Index: 95.4 to 96.8

Sentiment index expected pretty flat at 96.1 in April versus

a low 95.8 in March.

India CPI for April (Tue 1600 IST; Tue 1030 GMT; Tue

0630 EDT)

Consensus Forecast, Y/Y: 3.8%

Consensus Range, Y/Y: 3.8% to 3.9%

The consensus looks for CPI slightly firmer at 3.80 percent

on year versus 3.40 percent in March.

US CPI for April (Tue 0830 EDT; Tue 1230 GMT)

Consensus Forecast, CPI - M/M: 0.6%

Consensus Range, CPI - M/M: 0.4% to 0.9%

Consensus Forecast, CPI - Y/Y: 3.8%

Consensus Range, CPI - Y/Y: 3.5% to 4.0%

Consensus Forecast, Ex-Food & Energy - M/M: 0.3%

Consensus Range, Ex-Food & Energy - M/M: 0.2% to

0.5%

Consensus Forecast, Ex-Food & Energy - Y/Y: 2.7%

Consensus Range, Ex-Food & Energy - Y/Y: 2.6% to 2.9%

The consensus sees CPI up 0.6 percent on month and 3.8

percent on year in April after gaining 0.9 percent and 3.3 percent on year in

March, showing ongoing energy price shock.

Wednesday

Australia Wage Price Index for First Quarter (Wed

1130 AEST; Wed 0130 GMT; Tue 2130 EDT)

Consensus Forecast, Q/Q: 0.8%

Consensus Range, Q/Q: 0.8% to 0.9%

Consensus Forecast, Y/Y: 3.3%

Consensus Range, Y/Y: 3.3% to 3.3%

Wages seen up at the same 0.8 percent on quarter in Q1 after

0.8 percent in Q4.

Eurozone GDP Revised for First Quarter (Wed 1100

CEST; Wed 0900 GMT; Wed 0500 EDT)

Consensus Forecast, Q/Q: 0.1%

Consensus Range, Q/Q: 0.1% to 0.3%

Consensus Forecast, Y/Y: 0.8%

Consensus Range, Y/Y: 0.8% to 0.8%

The consensus sees no change from the last report with GDP

up 0.1 percent on quarter and up 0.8 percent on year in Q1.

Eurozone Industrial Production for March (Wed 1100

CET; Wed 0900 GMT; Wed 0500 EDT)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: -0.5% to 0.5%

Consensus Forecast, Y/Y: -1.8%

Consensus Range, Y/Y: -2.6% to 0.5%

Output seen up 0.4 percent on the month and down 1.8 percent

on year.

US PPI-Final Demand for April (Wed 0830 EDT; Wed 1230

GMT)

Consensus Forecast, PPI-FD - M/M: 0.5%

Consensus Range, PPI-FD - M/M: 0.4% to 0.7%

Consensus Forecast, PPI - Y/Y: 4.8%

Consensus Range, PPI - Y/Y: 4.2% to 5.0%

Consensus Forecast, Ex-Food & Energy - M/M: 0.3%

Consensus Range, Ex-Food & Energy - M/M: 0.2% to 0.3%

Consensus Forecast, Ex-Food & Energy - Y/Y: 4.3%

Consensus Range, Ex-Food & Energy - Y/Y: 3.9% to 4.3%

Consensus Forecast, Ex-Food, Energy & Trade Services

- M/M: 0.3%

Consensus Range, Ex-Food, Energy & Trade Services -

M/M: 0.2% to 0.3%

PPI-FD seeing energy price effects with a big 0.5 percent

rise expected on month and a whopping 4.8 percent on year.

Thursday

UK Monthly GDP for March (Thu 0700 BST; Thu 0600 GMT;

Thu 0200 EDT)

Consensus Forecast, M/M: -0.1%

Consensus Range, M/M: -0.2% to 0.2%

After a remarkable 0.5 percent jump in February, forecasters

see a 0.1 percent contraction in March.

UK GDP for First Quarter (Thu 0700 BST; Thu 0600 GMT;

Thu 0200 EDT)

Consensus Forecast, Q/Q: 0.5%

Consensus Range, Q/Q: 0.3% to 0.6%

Consensus Forecast, Y/Y: 0.9%

Consensus Range, Y/Y: 0.8% to 1.4%

The consensus sees a decent 0.5 percent rise on quarter and

0.9 percent on year.

US Jobless Claims for Week 05/09 (Thu 0830 EDT; Thu

1230 GMT)

Consensus Forecast, Initial Claims - Level: 208K

Consensus Range, Initial Claims - Level: 205K to 210K

The consensus keeps expecting claims to tick up, this week

to 208K from 200K last week.

US Retail Sales for April (Thu 0830 EDT; Thu 1230

GMT)

Consensus Forecast, Retail Sales - M/M: 0.5%

Consensus Range, Retail Sales - M/M: -0.3% to 0.8%

Consensus Forecast, Ex-Vehicles - M/M: 0.7%

Consensus Range, Ex-Vehicles - M/M: 0.3% to 0.9%

Consensus Forecast, Ex-Vehicles & Gas - M/M: 0.4%

Consensus Range, Ex-Vehicles & Gas - M/M: 0.1% to

0.6%

Rising gas prices again expected to boost nominal sales

growth to 0.5 percent overall.

US Imports and Export Prices for April (Thu 0830 EDT;

Thu 1230 GMT)

Consensus Forecast, Import Prices - M/M: 1.0%

Consensus Range, Import Prices - M/M: 0.8% to 1.1%

Consensus Forecast, Import Prices - Y/Y: 2.9%

Consensus Range, Import Prices - Y/Y: 1.1% to 3.2%

Consensus Forecast, Export Prices - M/M: 1.1%

Consensus Range, Export Prices - M/M: 1.1% to 2.0%

Fuel prices expected to lift both import prices (1.0

percent) and export prices (1.1 percent) on the month.

US Business Inventories for March (Thu 1000 EDT; Thu 1400

GMT)

Consensus Forecast, M/M: 0.3%

Consensus Range, M/M: 0.2% to 1.0%

A rather robust 0.3 percent increase is the call.

Friday

Japan PPI for April (Fri 0850 JST; Thu 2350 GMT; Thu

1950 EDT)

Consensus Forecast, M/M: 1.0%

Consensus Range, M/M: 0.5% to 1.3%

Consensus Forecast, Y/Y: 3.2%

Consensus Range, Y/Y: 2.8% to 3.7%

Japan's producer inflation, measured by the corporate goods

price index (CGPI), is expected to rise in April at the fastest pace in a year,

driven by gains in oil-derived products such as chemicals and in nonferrous

metals amid persistent geopolitical tensions in the Middle East, which have

disrupted shipments through the Strait of Hormuz.

The yen's weakness is also pointing to a re-emergence of

inflationary pressure through higher import prices. Given this backdrop, the

CGPI is expected to rise 3.2 percent on the year in April, the highest since a

3.9 percent increase in the same month in 2025. The index was up by 2.6 percent

in March after slowing to a near two-year low of 2.1 percent in February.

In March, the annual increase was driven by worsening Middle

East conditions and higher transaction prices for agricultural, forestry and

fishery products. Food and beverages rose 4.3 percent on the year,

agricultural, forestry and fishery products increased 18.9 percent, and

nonferrous metals surged 31.1 percent.

On a month-on-month basis, the CGPI is expected to rise 1.0

percent in April after increasing 0.8 percent in March.

Canada Housing Starts for April (Fri 0815 EDT; Fri 1215

GMT)

Consensus Forecast, Annual Rate: 240K

Consensus Range, Annual Rate: 230K to 240K

Starts expected up to 240K rate in April from 236K in March.

US Empire State Manufacturing Index for May (Fri 0830

EDT; Fri 1230 GMT)

Consensus Forecast, Index: 7.8

Consensus Range, Index: 4.0 to 9.0

Business activity expected to maintain moderate pace of

expansion with the index at 7.8 in May versus 11.0 in April.

US Industrial Production for April (Tue 0915 EDT; Tue

1315 GMT)

Consensus Forecast, Industrial Production - M/M: 0.2%

Consensus Range, Industrial Production - M/M: -0.4%

to 0.4%

Consensus Forecast, Manufacturing Output - M/M: 0.1%

Consensus Range, Manufacturing Output - M/M: 0.0% to

0.1%

Consensus Forecast, Capacity Utilization Rate: 75.8%

Consensus Range, Capacity Utilization Rate: 75.6% to

76.0%

Forecasters look for a modest 0.2 percent increase in

industrial production in April after a 0.5 percent decrease in March. Capacity

utilization expected nearly flat at 75.8 percent from 75.7 percent in March.

|